Genie Energy: A quirky allocator?

Genie Energy (NYSE: GNE, $6.48) is primarily an energy retailer (we’ll ignore their side hustles for now). It’s simultaneously a great business and a terrible one. It requires very little capital to grow and with its enormous operating leverage it prints cash during the good times. But it’s also a terrible business, as a mere reseller of commodities with no IP of its own. Either their own or their competitors’ poor pricing or marketing decisions can sink the economics and the company.

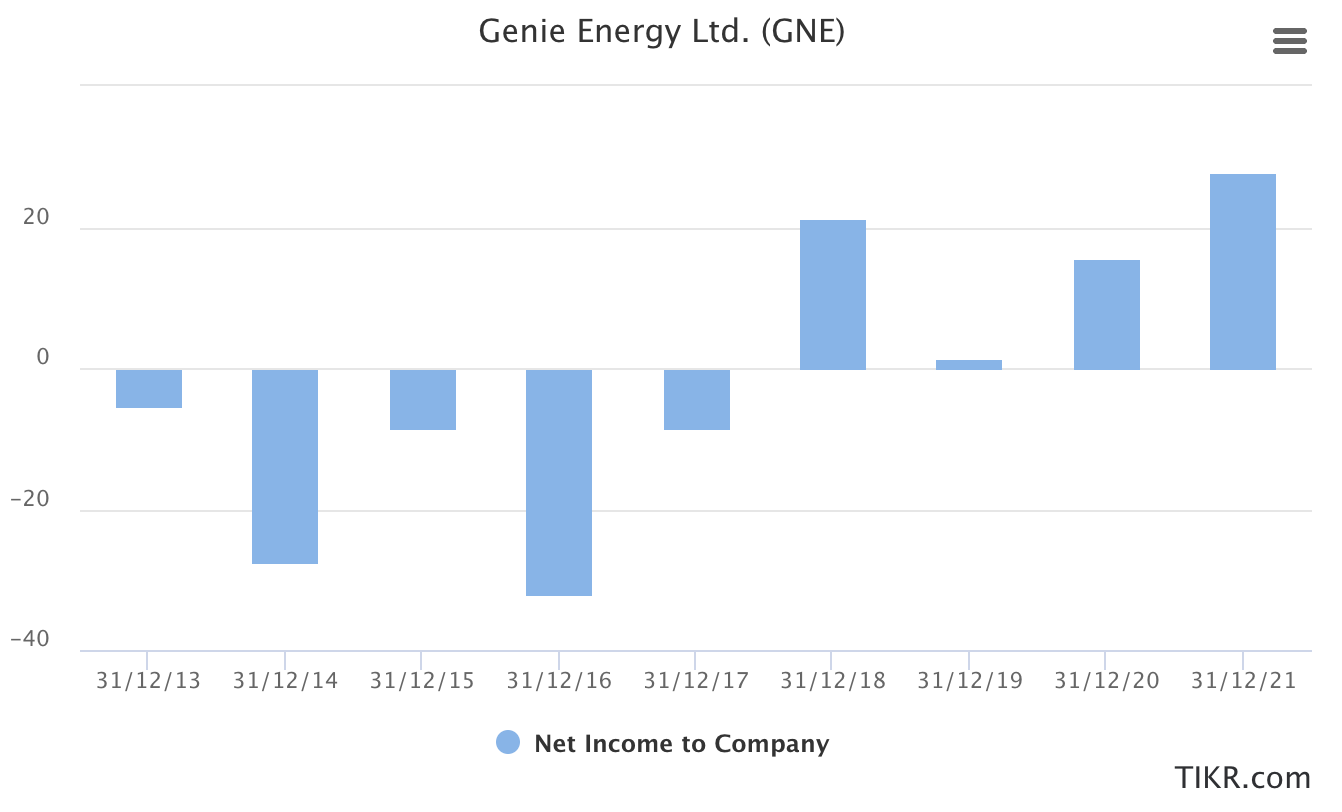

I got interested in May 2021. Genie had just reported a large loss during its first quarter driven entirely by large storms in Texas and Japan. They weren’t fully hedged and by selling at fixed prices to their customers they had to eat large increases in wholesales energy costs. The stock had been up close to $9 with a market cap of $220m, and the $13m profitability impact of the storm sent the stock down to below $6, reducing the market cap by around $55m.

There were several things to like. Firstly Genie passed on the sentiment check, where the outsized share price response to a clear one-off made no sense. They’d also just cancelled what had been a fairly high dividend after seven straight years.

Genie is a very entrepreneurial and opportunistic business. They have started or bought several small businesses which were in various stages of maturity and profitability. This isn’t surprising given they are chaired by Howard Jonas, a very strong capital allocator, with good insider ownership by him and the CEO.

Despite several loss making subsidiaries dragging on profits throughout the past few years, they were lumpily but steadily generating higher revenue, gross margins and net profit. Their investments were working but their reported financials were still reflecting the burdens of bets that hadn’t paid off.

The balance sheet was super conservative, with $40m of cash on the books. They had been shareholder friendly in the past, paying a decent dividend and buying back a little stock, and were exploring a spin off of their European operations until their UK business blew up.

There was also a consistent thread of discipline and long term focus throughout management commentary. This is crucial in a business where you’re essentially buying customers (or meters, as they are even less personally defined in the disclosures). Growth makes sense at some prices and it doesn’t at others. Some customers make more sense to acquire than others. Genie’s management understands this and they have articulated a sensible approach to growth.

On my numbers, this appeared to be a business on a 10-11x multiple of normalised earnings with undue short term pessimism and a clear road to increased profitability and resumed dividends. For those reasons I’ve been a shareholder since May 2021 at around $5.80. I expected to be waiting until at least year end FY22 to see any operational progress once the storms had dropped out of the financials. How wrong I was.

A few quick numbers to highlight what has transpired since:

- Current market cap: $170m (plus about $20m of preferred stock)

- Cash and marketable securities at at end of Q1’22: $95m (+$55m in 15 months)

- Enterprise value: Roughly $100m

- FY21 earnings: $29m

- FY22 Q1 earnings: $17m (though they’re highly seasonal)

- Dividends resumed at a 4.7% yield

- Buying back the prefs, though only at $1m per quarter

The lumpiness of the business makes forecasting very difficult, but it’s pretty reasonable to expect Genie to produce at least $30m of net profit this year. They’ve also got plenty of room to grow further in both their existing energy retailing business, with many untapped states in the US and adjacent markets in Europe, as well as their nascent solar generation business.

Right now we’re in the good times and the stock appears exceedingly cheap on recent earnings. It remains to be seen whether that will continue but the valuation, balance sheet, management, capital allocation and operational progress are all pointing in the right direction.

On the downside, I can’t forecast what the business is going to do apart from knowing that it has been on a long term positive trend. I can't even explain how profits have improved so much outside of repeating a couple of pithy sentences in their earnings calls. Guidance is patchy and the historical results have been extremely lumpy, relying on energy pricing, hedging and contracts into which investors have very little insight. While I’m including the influence of Howard Jonas and his past success on the positive side of the ledger, there are also enough related party transactions that you have to just accept you’re along for the ride with him.

I always get more interested when there are obvious but superficial reasons to overlook a company. The short term profitability issues and dividend cut need no explanation. I believe (though I’m not certain) that Howard Jonas’s related party dealings also fall into that category. How the business makes money is simple but the actual results are not intuitive. There’s no mainstream analyst coverage.

The list goes on. Genie management at first glance appear disinterested in external shareholders. They produce really fugly investor presentations which tell you they’re spending the appropriate amount of time on investor relations. In a recent earnings call (minute 27), the CEO hilariously tells a shareholder, ‘Go sell.’ (Curiously, this was excluded from the transcript.)

While these factors might dissuade others, I believe it’s a reflection of the internal scorecard and convictions of management, who are not trying to hit quarterly numbers or making decisions based on investor pressure. (It helps that there isn’t any – the mere receipt of the question linked above was quite an aberration.)

All I can say is that so far it’s worked. Jonas has been a dealmaker and an allocator from the beginning across several different businesses, and Genie’s cash pile, various ventures and valuation make this a very good setup in my view.

Disclosure: I own shares in Genie.