How can these prices be right?

I buy international and typically emerging market stocks because they can be much, much cheaper than corresponding developed market stocks. For this post I’ve paired up a couple of side by side comparisons of developed market stocks with their better-known developing market peers.

I’ve intentionally chosen extremely high quality businesses. There can be no argument about the businesses themselves and most of the valuation difference must then come down to economic, competitive, regulatory and governance factors.

The sheer size of the valuation gaps are sometimes astonishing. Should Polish and Russian businesses really deserve to trade at one-third and one-sixth of developed market peers? I don’t think so.

ASX versus GPW

First up is ASX ($93.02), Australia’s stock exchange. Stock exchanges are truly among the best businesses in the world and it’s apparent in ASX’s financials. ASX boasts an NPAT margin of 47% which has grown almost without interruption for approaching 20 years.

The GFC and Covid had barely-perceptible impacts on its profitability and there’s no realistic scenario in which the various markets that they oversee are taken elsewhere any time soon.

No surprise then that it trades on 35x earnings and a 2.4% dividend yield.

I struggle though to see how the business is that different to Giełda Papierów Wartościowych w Warszawie (GPW, zl43.20), Poland’s main stock exchange operator, outside of the typical investor’s inability to pronounce it (myself included).

They operate a similar range of markets and have equivalent financials. GPW’s NPAT margin is 39% and ROE is even better at 19%. Growth has been lumpier but materially faster than ASX over both five and ten year periods.

Now, I don’t consider myself an expert business analyst and, with an investment strategy that’s as close to assembling a tightly screened ETF as it is to active management, I am certainly not your best source of insight on the competitive and strategic details that distinguish these two businesses. But to me these are essentially the same business.

You could absolutely quibble about the details. GPW has some debt. It’s in Poland. Overall the earnings are high quality, but you could shave 10% off due to some equity accounted subsidiaries. Some divisions have grown over time, some are withering. I’ve taken only a quick look at the investor presentations and I’m sure one could find more reasons to not to like if you wanted to.

The biggest distinction is that GPW trades at 11x earnings versus ASX’s 35x, and its dividend yield is 5.7% versus 2.4%.

This may seem superficial but I really struggle to imagine what qualitative or competitive scenarios might bridge the gap. If the discount instead reflects the business being in Poland I also don’t get it. I can think of more risks for ASX than GPW.

ASX’s five and ten year NPAT growth rates are 2.4% and 3.1% respectively. Given inflation rates hovering around 2% in Australia over those periods it’s hard to argue this is a growth stock. A re-rating seems a serious risk at some point. If the argument is that it’s priced like a bond rather than a growth stock, the same risk applies and seems heightened given current inflation concerns.

Who knows when multiple compression might occur, but with a 3% earnings yield growing in line with inflation, there’s plenty of time for the world to change before you’ve gotten your money back.

In terms of upside, Australia is one of the most financialised countries on the planet meaning ASX must surely have less runway for growth. Its market cap of A$18bn looks pretty juicy to all manner of fintechs who could shave just a little slice off the side and have a great business.

At least to this know-nothing value investor, GPW seems to have more upside. Poland’s stock market capitalisation to GDP is variously reported around 40% versus Australia’s at around 120%, and there’s also more room for GDP to grow. GPW’s market cap is a mere A$600m equivalent which is a much smaller prize for competitors to chase.

To address the corporate governance question investors typically have with countries they know little about, consider for the moment that this is Poland’s stock exchange. GPW’s entire existence revolves around creating markets that investors want to invest in. Any rational manager of that business would want their company to be a good role model. Dividends have flowed for 10 years straight.

Lastly if you're sceptical of Poland’s economy, consider that their central bank has hiked rates from 0.1% to 1.25% in the two months to November 2021 in the face of rising inflation. We are certainly not seeing that monetary discipline in Australia.

GPW is certainly not my best idea, but GPW versus ASX is an absolute no brainer for me.

Disclosure, GPW is one of my smaller positions bought at zl44.

Qiwi versus PayPal

Qiwi Plc (QIWI, $8.99) is a Russian payments business and as far as I can tell its closest equivalent in the US is PayPal (PYPL, $202.03). If you know the space well, feel free to chuckle at my ignorance and substitute in your favourite overpriced payments business. It’s a serious business with payment terminals in 120,000 points of sale and 20m digital wallets.

Qiwi ticks many of the boxes that allow most investors to rationalise not investing in places like Russia:

- Russia’s newly created gambling regulator recently appointed Qiwi’s competitor to be the new monopoly provider of payments services for gambling. If I’m reading the disclosures correctly 15% of Qiwi’s total revenue will disappear as a result. The process seemed pretty opaque and I’ll let you guess as to why the regulator thought a monopoly provider was necessary.

- In 2020 another regulator halted Qiwi’s processing of payments for foreign merchants along with many of its competitors and turned off part of the business overnight. I believe that's since been relaxed but customers have presumably found workarounds in the meantime.

- Qiwi’s physical POS and digital wallet counts were down -20% to -25% in FY20.

- They’ve lost 2 CFOs in a couple of years due to ‘personal issues’ and have a new CEO.

- The Ruble’s depreciation in 2014 chopped profits in half.

I won't go into PayPal's virtues, but suffice to say some discount to PayPal is obviously warranted. Let’s level set with PayPal’s key valuation metrics (financials are to 30 June 2021):

- Market cap: $142bn

- Price / revenue: 6.0x

- PE: 29x

- P/B: 6.8x

- Yield: Donut

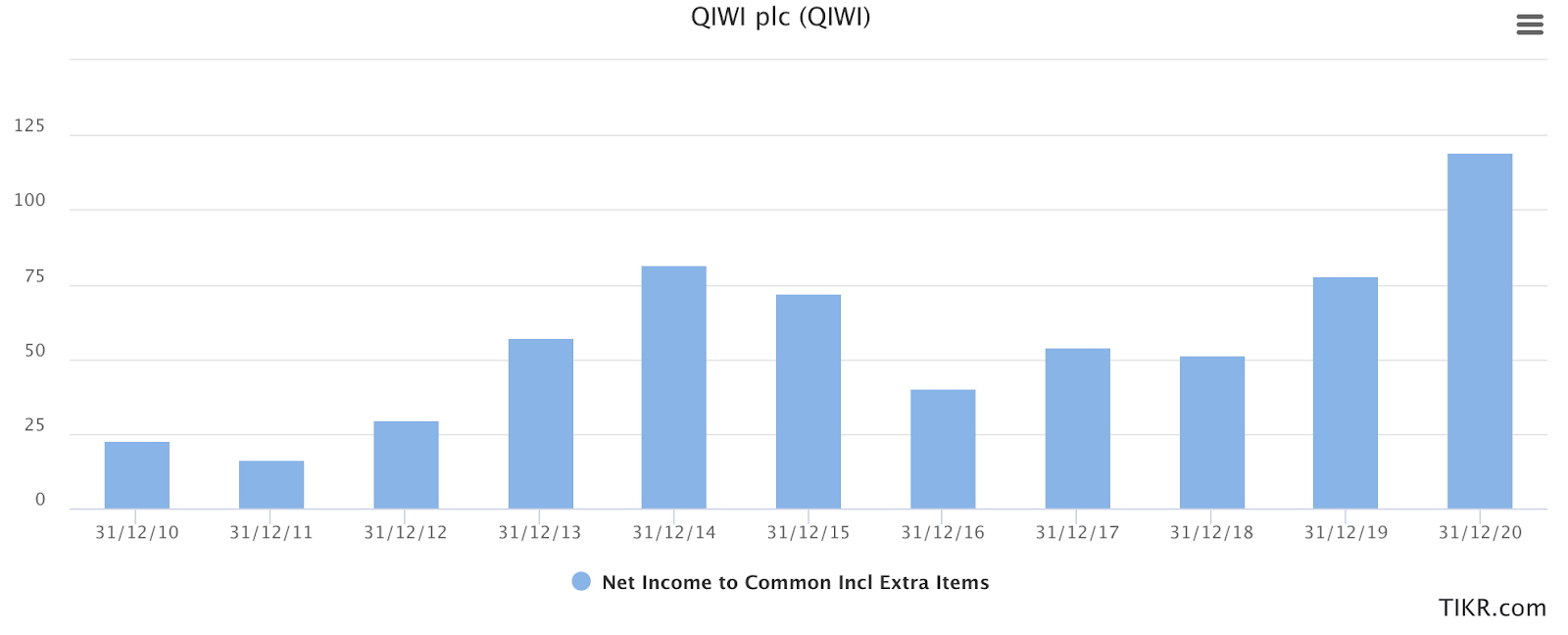

So what’s a reasonable valuation for Qiwi in the context of the profit growth below? Keeping in mind:

- Guidance for a one-off decline of around 25% in FY21 due to the aforementioned regulatory hits

- This is USD profit and already accounts for the fact that the Ruble has halved over this period.

One could apply various discounts for corporate governance, regulation risk, double count the currency risk and throw in a few other things as well. No matter how imaginative you are with various risks and applying discounts, I think it’s worth more than this:

- Market cap: $560m

- Price / revenue: 1.0x

- PE: 3.8x

- P/B: 1.2x

- Yield: 15%

As mentioned the regulation impacts are still to be felt, but regardless Qiwi is trading around one-sixth of the price of PayPal. Perhaps my simple value investor brain is missing something, but that seems perhaps too big a discount.

I’m eyes wide open to the risks. I purchased in early June at $10.85 when it was known that Qiwi was one of two horses in the race to be the monopoly gambling provider. When they announced the loss their announced revenue impact was almost double what I had estimated.

The risks are real. But the price makes it pretty difficult to lose a lot of money over the long term, as does the 15% yield (though I'm assuming at least a temporary reduction).

Like GPW, there are plenty of upside opportunities. A mere relaxation of ongoing regulatory impositions would increase profits and sentiment. The share price tells a story of risk but also the potential for reversal. Qiwi’s PE has declined from ~40x to 4x, and price to revenue has declined from over 5x to 1x. But emerging market multiples expand sometimes too.

The Ruble has been a constant headwind for as long as time. At the risk of showcasing complete ignorance, I think there’s a good argument that the Ruble is now undervalued.

The Big Mac index is laughably superficial, but it tells you something. It tells you that something very quickly. It’s also free and easily available, and most importantly it doesn’t trick you into thinking you know more than you do.

The Big Mac index typifies my approach to information gathering, which is that incremental information has hugely diminishing returns, and that knowing the limitations of your information and your forecasting ability is much more important than having more or better information.

I could read all manner of analysis on currencies, I could even do a PhD on the Ruble, but I don’t think my takeaway would be much different from a five second eyeballing of the charts below: The Ruble is cheap both against other currencies and in relation to its own historical discount to other currencies. In a world where oil and gas may again be finding favour, it could be very cheap.

A threefold and a sixfold difference in valuation for pairs of very similar businesses demands serious explanation. You shouldn’t need to look. I couldn’t find it.

You could disagree with me about which of these businesses is too expensive or too cheap. But the prices of these four stocks cannot be right.