I Reckon

Let me present an exciting new SaaS opportunity to you. It is a mission-critical piece of software with extremely sticky customers which every business on the planet needs. It’s been around for decades and has been profitable throughout. Profit grew during Covid. It makes $9m of profit growing 8% per year (3 year CAGR) on $75m of revenue.

What would you pay for this business? 30x earnings? 30x revenue?!

Oh, you’re talking about Reckon, that crappy accounting software business getting crushed by Xero? In that case, 12x earnings and 1.5x revenue.

Reckon is the epitome of deeply entrenched expectations. The narrative that was created in 2015 was one of an incumbent that didn’t get its cloud transition right, which was steamrolled by more nimble and better funded competitors, which is gradually fading into irrelevance.

The story is not entirely wrong. Reckon is certainly not the company that it once was and it may never return to its previous levels of profitability:

But that was five years ago. Reckon has passed through the valley of death (while remaining quite profitable throughout, mind you) and I’d argue it’s a much safer investment than its more esteemed peers.

Reckon is a cockroach which has been stomped all over and has done just fine. That damage is now in the past. The future should be not worse than the past, and it could be much better.

Let’s revisit the various elements of the narrative and see whether they need updating.

Reckon hasn’t made the cloud transition

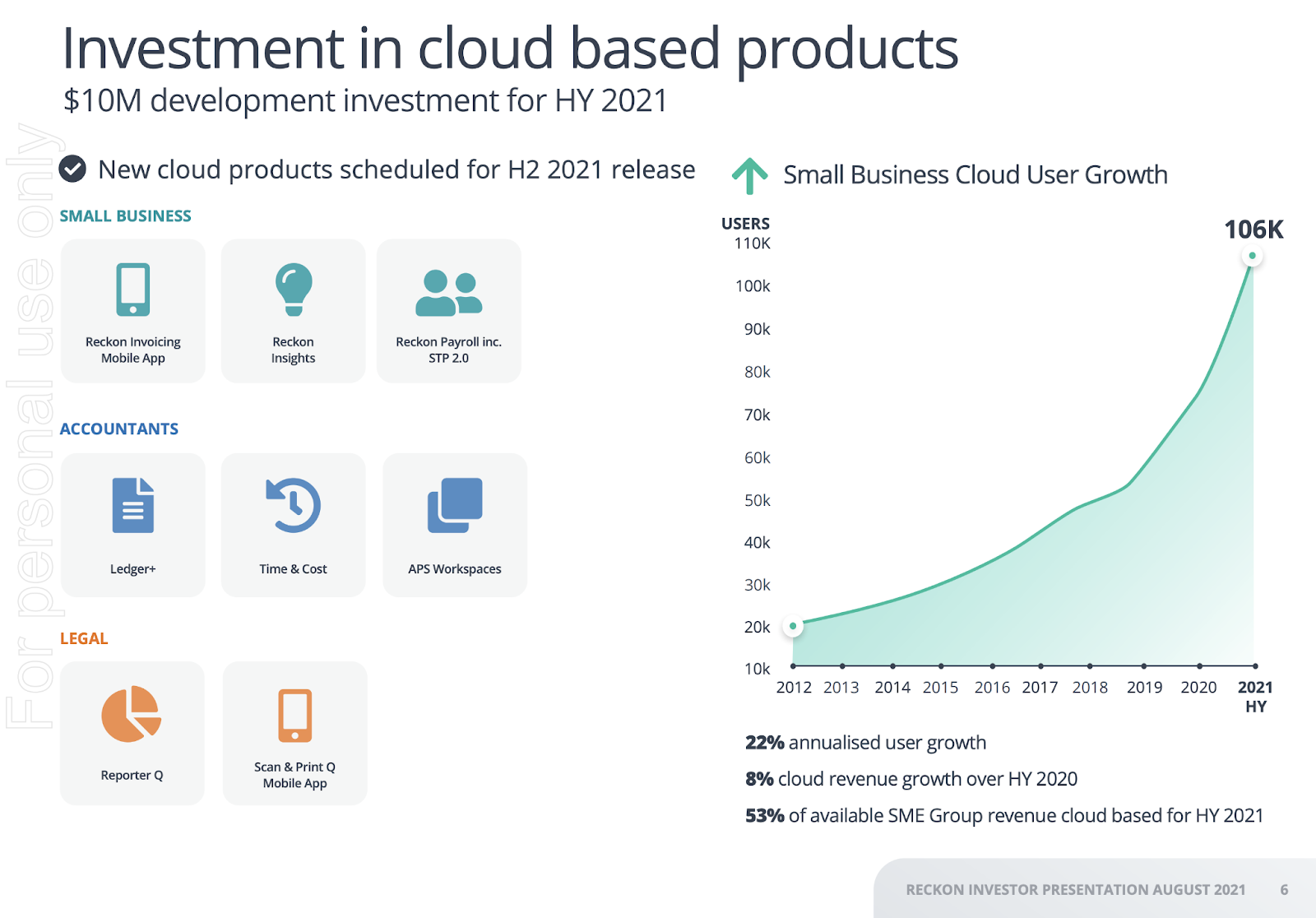

Reckon hasn’t completed its cloud transition. There’s still work to do on products to enable it. But the hard part is done.

Reckon have been stuck in the ‘pain today’ part of the process — maintaining its legacy products while building an entirely new product suite in parallel and less than half of their customers have transitioned. They’re now in ‘gain tomorrow’ mode; enjoying both the transition to higher ARPU for cloud products on existing customers, while opening up to new customers now they have a real cloud offering.

Its SME division, accounting for 55% of total revenue, generates half its revenue from cloud software.

Only 6% of its practice management customers have switched so far and by the sounds of things the product is not complete enough for all customers to switch to. But it’s picking up steam.

There is of course churn risk as the transition occurs, particularly for the practice management division which is about one third of revenue. But there is at least as much opportunity as there is risk.

So I'm calling this busted. Though it has not completed the transition, Reckon has built the products and is shifting customers.

Reckon is the incumbent

In 2015 Reckon was the incumbent milking their legacy desktop business. Xero’s offering was genuinely much better and it made absolute sense for customers to switch. Xero could invest heavily to capture greenfield revenue growth. Reckon, on the other hand, saw revenue fall and had to play catchup on the product side.

But who is the incumbent now? Which of these two businesses could hurt the other?

Xero was the disruptor in 2016. But today it can’t compete any harder and it’s got much more to lose.

(I’m using Xero as the specific example and, without having done the work, am assuming this broadly applies to the rest of the market. I can’t be too wrong here given how large a component of that market Xero is. Also, more than half of Xero’s revenue comes from Australia and New Zealand so the comparisons don’t need much adjustment.)

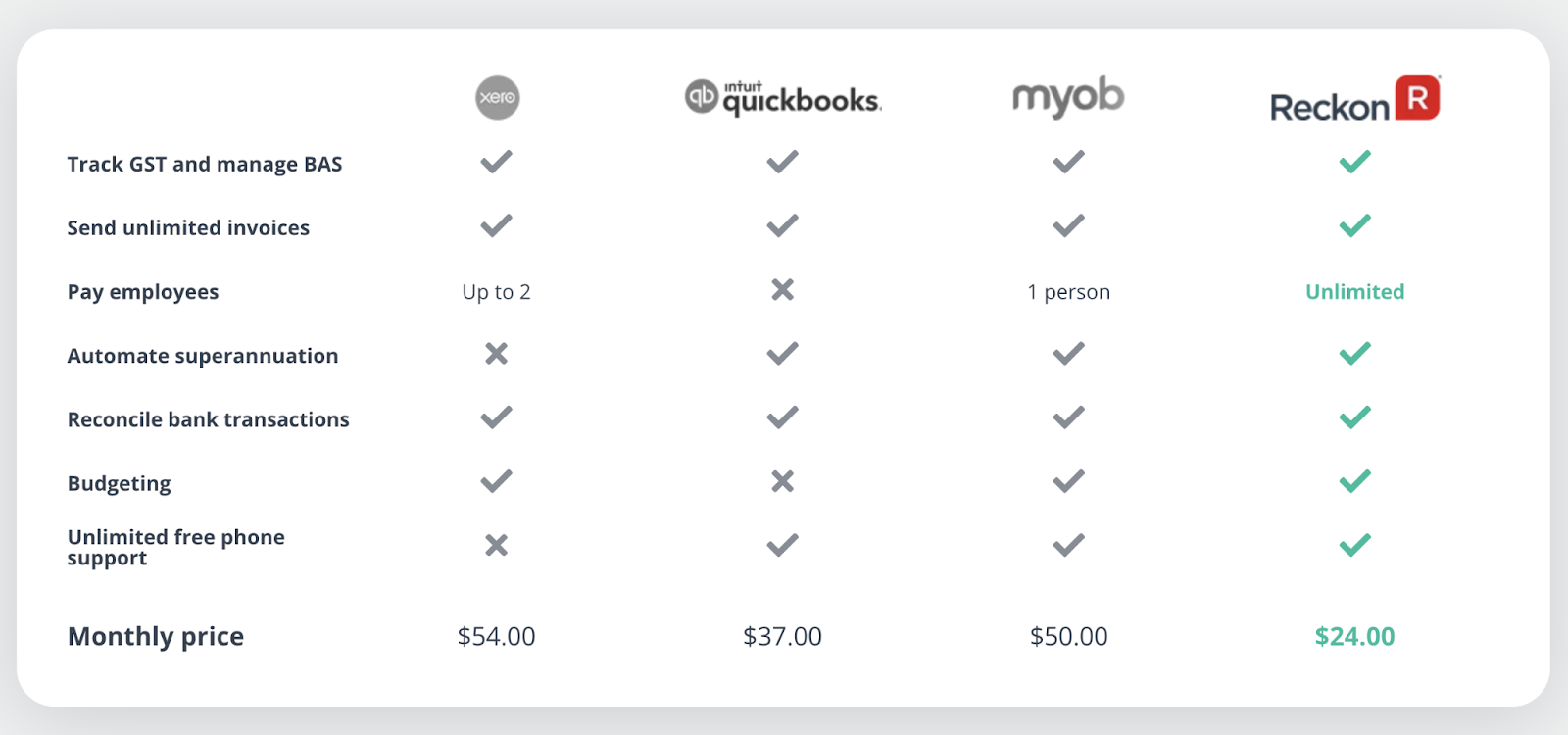

Reckon are the lowest cost provider in the SMB accounting software market. Xero can’t cut prices because it’s scarcely profitable, it has a much larger revenue base to protect and a revenue decline would cause a bloodbath for its stock price. Price cuts are much more costly to Xero than to Reckon.

Secondly, Xero spent $300m on marketing last year (36% of revenue) compared to $3m at Reckon (4% of revenue). What could Xero do, double spend to $600m (70% of revenue)? Again, Xero would be much more severely impacted by a marketing war than would Reckon.

There are plenty more levers that Xero could pull than price and marketing but they tell you something. I struggle to see how competitive intensity could get materially worse (at least from the established players in the list above). If it doesn’t get any worse then Reckon can continue chugging along profitably as they have been, accepting their place in the market and doing well.

There’s also a scenario in which competitive intensity relaxes and Reckon finds growth easier to come by. That might not happen, but if it does it could be the difference between no growth and moderate growth for Reckon.

Reckon have been displaced. But it's over. That will no longer weigh on their future results. They have accepted their new role as the scrappy little competitor and have adapted well. That means their current $10m of earnings is higher quality and probably deserves a higher multiple than in 2015 when it traded at 15x.

Xero are crushing Reckon

This one is easy:

Xero:

- Market cap: $22bn

- Aggregate 5 year profits: -$92m

Reckon:

- Market cap: $110m

- Aggregate 5 year profits: $33m

Xero, despite having a market cap 200x that of Reckon, has only been more profitable in one year. This is a little tongue in cheek, I get that Xero is investing through the income statement, LTV > CAC, they could be profitable if they wanted etc etc.

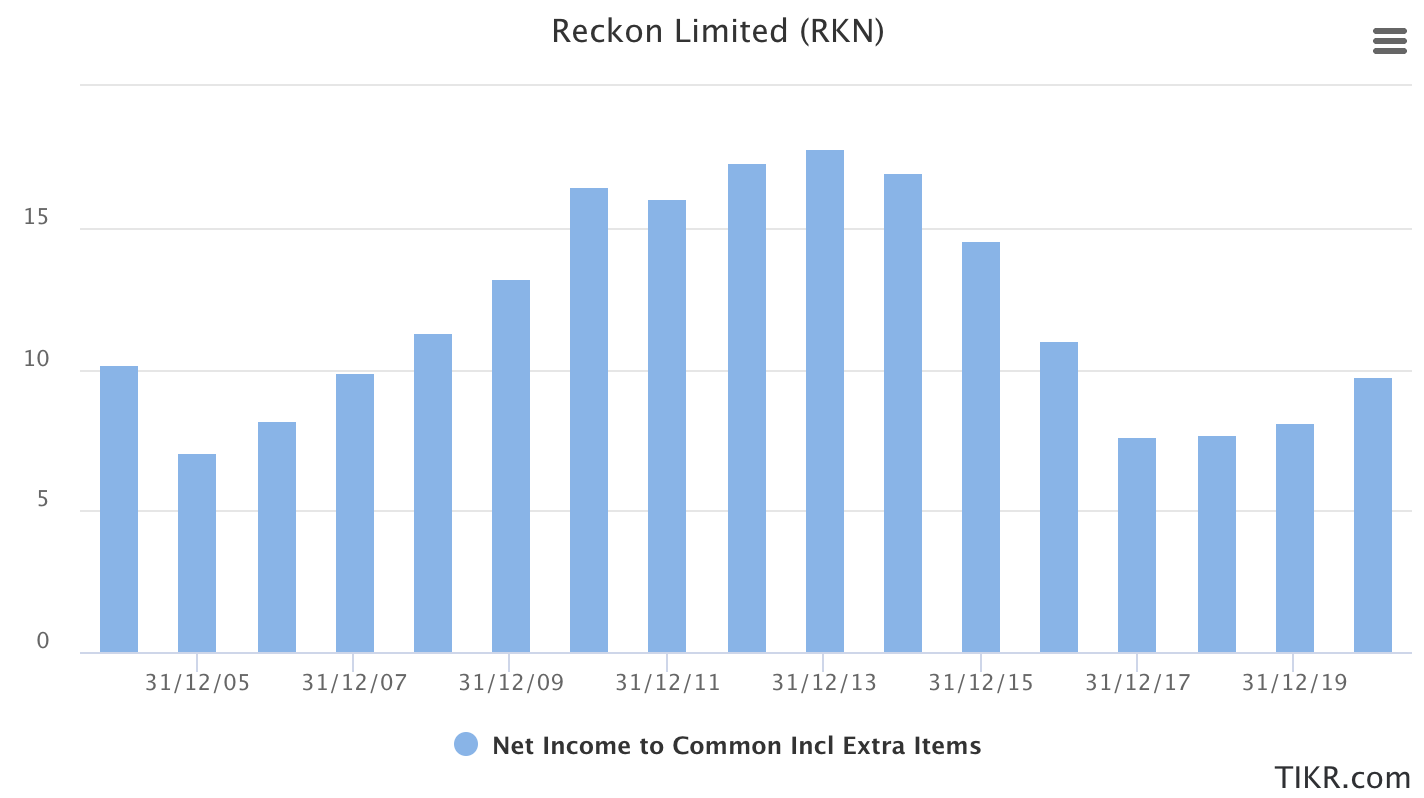

But despite the narrative of complete disruption, Reckon continues to do just fine. Profit is down to $10m from a peak of $18m. They’ve been profitable every year that I have data for, back to 2004.

I think this clearly demonstrates the strength of Reckon. Billions of dollars of capital have been thrown into direct competition with it, and it has managed to sidestep most of the damage and continue to print money. Like I said, this is a cockroach.

There’s no growth

So the narrative is true here. There is no growth. Revenue has been stuck at an annual run rate of about $75m for three years. Profits have done a bit better but nothing to write home about.

The point though is that a turnaround in revenue — anything at all — will generate the operating leverage that makes SaaS businesses so wonderful. That ran in reverse for several years as seasoned shareholders would be all too aware. But this can go in the right direction for Reckon as well.

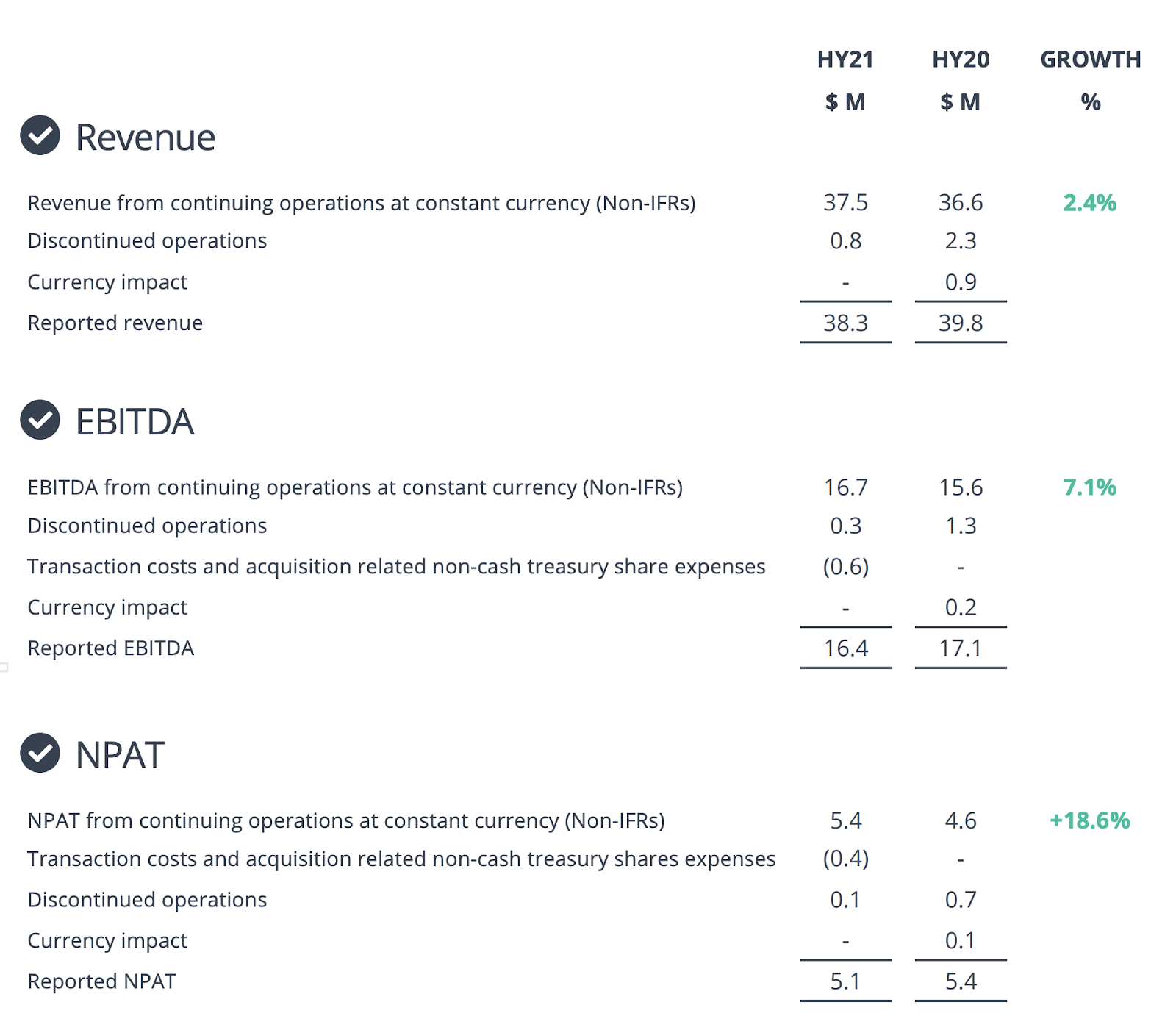

You can see this in the most recent half year results. A mere 2.4% increase in revenue generated a nearly 20% increase in NPAT as it should for a business with fixed costs and a current NPAT margin of 15%.

Now, a H1 result does not a turnaround make. But it suggests at the possible upside, the potential for very, very slight revenue increases to translate into profit growth, but even more importantly, into a new narrative of growth.

Why I like it

I’m not often overwhelmed with vehement agreement while reading management commentary, but I like that Reckon's management have archaic values like, you know, generating a profit and eschewing value-destructive growth.

Their CEO seems sensible and is consciously moving towards less competitive markets. This is the right way to play Reckon’s hand.

"We've had to move away from a direct competition with the likes of MYOB and Xero ... We run our own race and we run a different business to MYOB or Xero, but their model is to throw a lot of money into things like marketing," he said.

"We have really good products, so it's about being smart and coming up with strategies to enter the market where we can get more penetration.

"We've also long said that we want to move into new markets that aren't as hotly competitive as the ones we've been playing in. Our first foray is into the medical sector ... and we've just signed a three-year deal with the Australian Physiotherapy Association, which represents about 80 per cent of the physios in Australia."

This rationality makes sense in the context of the board and management owning 19% of the business and caring about cash flow rather than their diluted market cap increase come the next capital raise.

They’ve also been making what look like sensible deals. They sold a small division to a close collaborator at a decent enough price and have merged in a small company, maintaining the key execs and incentivising them well. It displays focus and an understanding that they want all their stakeholders to make good money from Reckon’s success.

At the current price, today’s investor will do okay if nothing gets any better for Reckon ever. They are within spitting distance of paying down their remaining debt. With no meaningful capital requirements they could soon pay a ~8% fully franked dividend yield, up from today's 5%.

There are plenty of other ways to make money too. MYOB announced it was buying Reckon’s practice management businesses for $160m in 2017. Though the deal ultimately fell through, this amounted to 160% of Reckon’s current market cap for a business contributing less than half of its revenue.

The more likely upside scenario though is that the narrative changes dramatically on just slightly better results.

Who is the natural buyer of a $110m market cap, unpopular, second-rate, no-growth company, with an obviously inferior product suite which earns less than it did in 2007? Most investors are not liable to seek this investment out. There’s no obvious change, no catalyst. It’s boring. 12x earnings is about the right price for a high quality but zero growth business.

But if a new narrative of growth is created, a material re-rating will occur. It would only take two years of 3-5% revenue growth generating 10-20% profit growth to make Reckon a $2 stock.

I don’t know whether that will happen. But I think 12x earnings is about the right price for Reckon with no upside potential.

Disclosure: Bought at $0.80 earlier this year, sold into the recent Novatti excitement and about to buy it back.