NEXTDC: Security analysis vs business analysis

I think of security analysis as the skill of mechanical, backwards-looking, Ben Graham-style investigation of stocks with a heavy quantitative focus, largely devoid of analysis of the business itself and what it does. Business analysis in my mind is its complement covering the softer side of analysis — management, competitive advantage and moats — which determine what the future’s numbers will look like.

It is conventional wisdom that security analysis has become less valuable. It’s too simple, too easily and widely practiced to provide an advantage to practitioners. It’s table stakes; necessary to play the game, but one shouldn’t expect to have an edge unless you have industry expertise as well.

I agree to a point. But investors can get far too wrapped up in business analysis and complex modelling and overlook the really obvious facts that security analysis provides.

Outside of microcaps and EM, I’m probably a below-average business analyst compared to my competitors on the other side of trades. But I think I’m a pretty good security analyst. By looking at a lot of stocks and with the consistent application of simple maths it’s often easy to spot stocks where business analysis has sent investors off the deep end.

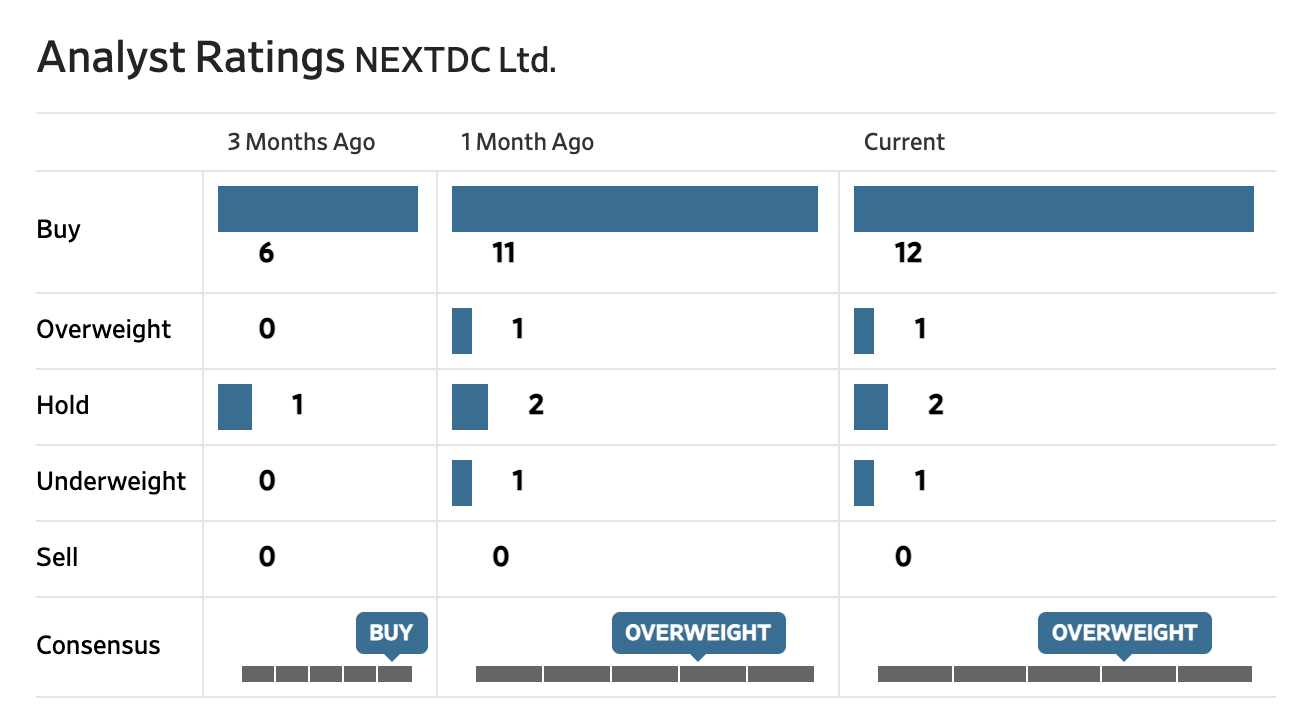

NEXTDC is a case in point. At $11.65 it’s a A$5.3bn business with 14 analysts covering it and overwhelmingly positive sentiment. In my view it’s very probably overpriced.

NEXTDC owns data centres (DCs). It’s a very simple business. It builds large buildings and lets its customers stick their computers inside. It keeps the servers cool and supplied with plenty of electricity. If that was all there was to it, this would be just another REIT.

Increasingly though, NextDC connects its customers’ servers to one another so that different cloud services can communicate between one another more efficiently. With thousands of customers and an ever-growing web of interconnections between their servers, the story goes that NEXTDC is building network effects which it’ll be able to better monetise over time.

From this point, the next step in valuing the business would seem to be corroborating just how valuable these network effects are. How could one put a price on this asset without knowing whether this is a REIT or a technology platform?

Well, before diving into that I’m going to take the shortcut method with some good old-fashioned security analysis. Let’s start with some basic figures. Today's $5.3bn market cap buys you:

- $246m of revenue

- $165 of gross profit

- -$21m of net profit after tax

- $1.6bn of equity

You’re obviously not buying this business for what exists today. NEXTDC trades at 3.3x book value because you’re buying the option to invest more money into assets that generate high rates of return.

Let’s work through how valuable the option to continue investing could be assuming historical returns continue.

NEXTDC 2017 investor day slides showed that early developments were earning around 20% returns on invested capital (defined as EBITDA on total capex). Putting aside the question of whether EBITDA is the right measure of return for a business which builds warehouse-sized server refrigerators, how does this translate into a return for you as an equity holder?

NEXTDC currently has $1.9bn of property and plant and $780m of debt so they’re gearing around 40%. They’ve got some cash as well for future expansion. Let’s assume they’ll spend all the cash and they’ll continue financing their property and plant with 40% debt as they have been. If they spend their $650m of cash and gear that up, they’ll have around $3.0bn in plant and $1.2bn of debt.

If they can continue making a 20% return on that capital, they’ll be generating about $600m of EBITDA. Make some (generous) assumptions about interest, tax and debt and I get to $460m NPAT for about a 12x PE once they're fully invested. Not too bad.

But that 20% return was for mature assets. They don’t start that way. There’s a ramp until the buildings fill up with customers and the connections are made. It’s not a 20% return if you have to wait 5 years for your 20% return to start flowing.

I don’t know exactly what the lag is, but it’s a long time. If you compare cash flow in any individual year to total PPE, you’ll see returns of 3-7% depending on the year. Not until you lag PPE by 3-4 years do you start seeing cash flow returns of over 20%. Since that includes contributions from younger assets and asset growth has been rapid, the lag must be at least 5 years.

Let’s model that out. Here I’m assuming NextDC build a $100m property, funded with $60m of equity and $40m of debt. It takes 5 years to ramp to a 20% EBITDA return on capital then grows more slowly for another 5 years before I take my terminal value.

As the maths shakes out, your 20% EBITDA on capital translates to an 18% IRR to equity after you subtract out the interest and tax, discount the future earnings, then dial the return back up for the gearing.

| Year | Capex | EBITDA | Owner earnings* | Discounted earnings |

|---|---|---|---|---|

| 0 | ($100) | |||

| 1 | $0 | ($0) | ($0) | |

| 2 | $10 | $7 | $5 | |

| 3 | $14 | $10 | $6 | |

| 4 | $17 | $12 | $6 | |

| 5 | $20 | $14 | $6 | |

| 6 | $21 | $14 | $5 | |

| 7 | $22 | $15 | $5 | |

| 8 | $23 | $16 | $4 | |

| 9 | $24 | $17 | $4 | |

| 10 | $156 | $108 | $20 | |

| $60 | ||||

| Terminal growth | 3% | |||

| Equity investment | ($60) | |||

| IRR | 18.4% |

I should point out that I'm really giving NEXTDC the benefit of the doubt here. Owner earnings assumes no capex ever, DA is 3% annually as a tax shield only, 30% tax rate. IRR to equity assumes 40% debt to PPE assets and 4% interest rate.They have made profits in some years but they have never come close to this modelled ROE given they've been in constant growth mode.

Anyway, assuming all available capital is put to work at 20% EBITDA returns, our modelling shows we should receive 18% returns on equity. And we’re buying $1.6bn of equity for $5.6bn. Hmm. So my $5.6bn company will only make me $295m of NPAT ($1600m * 18%), or a 5.2% return on my purchase price?

That’s where the value of the option comes in. You only buy $0.29 of book value for every $1.00 you invest at today's market cap. The hope, your only hope as an investor in this business, is that NEXTDC continues to raise and deploy more capital. If that doesn't happen, then expect a return of no more than 5.2%.

Additional contributions will add $1.00 of book value for every $1.00 you part with, which averages up your starting point of $0.29 of book value for every $1.00 of ownership. (In reality you don't need to actually contribute the capital yourself. If NEXTDC can raise equity capital without diluting your ownership you get the same result.)

So how much capital needs to be added?

If you want a 10% return as a shareholder and management are investing at an 18% ROE, you have to keep committing more equity into the business until every $1 you’ve invested is backed by $0.55 of equity capital (18% ROE * $0.55 book = $0.10 return per $1.00 invested).

| Market value | Book value | $ of book per $ market value | Return to owner | |

|---|---|---|---|---|

| Current value (m) | $5,600 | $1,600 | $0.29 | 5.2% |

| Additional contributions (m) | $3,400 | $3,400 | $1.00 | 18% |

| Total capital (m) | $9,000 | $5,000 | $0.55 | 10% |

That means shareholders must kick in an additional $3.4bn of equity capital, or another 200% on top of what has gone into the business to date.

Management must then gear it up and build more facilities. Leveraging that $5bn of book value will support about $8bn of property and plan. So management must grow today’s $1.9bn of property and plant by over 4x for you to earn a 10% return.

Is it possible for NEXTDC to invest that much while still earning 18% on equity, while several other players are doing exactly the same thing? I have no idea. But it's certainly not a given. If you are willing to make that bet, I hope you’re a really good business analyst.

Growing industry-wide data centre capacity by more than 4x is no joke. Further, the demand for incremental data centres requires growth on top of growth. Those DCs house servers which get faster and consume less power every year. If another DC never got built, we’d still have rapidly growing compute capacity within existing DCs as the hardware continually improves.

Renting space in a DC is a very low marginal cost operation once it's been built. Low marginal costs + oversupply = big price falls. God help shareholders if the industry overbuilds.

On that front, it seems a near certainty that there will be an overshoot. This is a hot, capital-rich growth industry, with long lead times, in which investors require and expect managers to build in order to make a return. That set of incentives will breed oversupply.

So it’s an interesting set of economics. As an investor in NEXTDC you require two things to go right:

- Returns to be maintained amidst copious supply addition

- Not be overly diluted as further equity is raised

Let’s assume for a second you’re safe on number #1. How does the company shape up on fairness in dilution when raising capital? It literally could not be any worse.

The CEO behaved so poorly last time they raised capital that it may actually provide some protective benefit because he surely could never be left to his own devices to commit such an egregious error ever again.

I didn’t know this story until researching the business, but the hilarious headlines from AFR tell some of what went on:

- Why NextDC's $672m raising leaves fundies furious

- NextDC's Craig Scroggie flunks investor relations 101

- NextDC board rolled by 'zeroed out' shareholders

The CEO, while undertaking a large placement during Covid (in excess of actual capital requirements mind you), literally went through a list of his large shareholders, picked some of his favourites and excluded some major shareholders based on his uninformed opinion of them.

This is not the person I would want at the helm when the investment case requires copious capital raising.

Realistically this isn’t going to impact the outcome too much. Even in a repeat of that scenario, missing out on a 15% discount for a 60-70% increase in shares isn’t going to be the difference between a good and bad outcome here. But it's another strike against NEXTDC as an investment.

Summing up, today’s investor must believe that modelled and yet to be realised ROE of 18% can be maintained while an exciting growth industry builds out multiples of its current capacity, keeping strong price discipline on its low marginal cost service, while hoping for fair treatment from a CEO who purposely allocated shares in such a way as to dilute shareholders he didn't like. If that all works out you can expect a 10% return from here.

I won’t be waiting on the register to see how this one turns out.

There is of course every chance that the share price moons in coming years as facility completions start flowing into the income statement, and it's not hard to imagine a super fund taking NEXTDC out. But I suspect a buyer paying today's price regrets it in a few years' time.

So that’s how I implement security analysis. A lot of simple maths, some general business knowledge and moving on quickly when valuation stacks the odds against me. Having gone through this process I still know nothing about data centres outside of what I read in NEXTDC's investor presentation. But I'm pretty sure it doesn't matter for making the right call here.